7 Trends Continuing into 2022 for Credit Unions

By Lydia Wedlock

For credit unions, 2021 could be considered a good year – certainly better than 2020. However, that one infamous year left behind a trail of financial destruction for both credit unions and their members, and while progress has been made, the damage hasn’t been fully repaired yet. And further changes could be on the horizon, so credit unions will need to be on their toes for the changes to come.

Looking for Lending

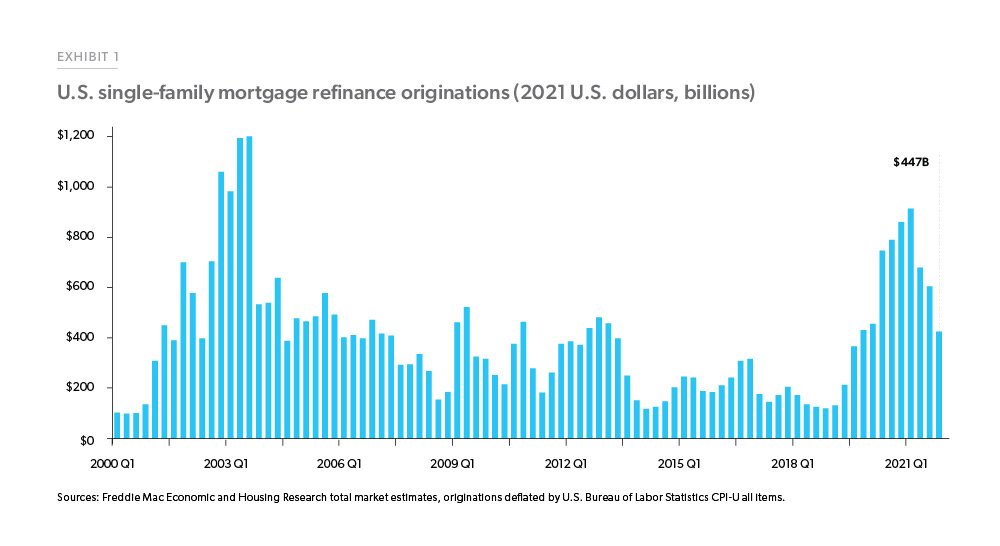

Last year was full of ups and downs in regard to lending. For example, mortgage refinancing saw a dramatic increase due to low interest rates, but generally speaking, these lower rates across the lending spectrum didn’t help credit unions in terms of profitability. Due to this lower profitability, having a successful and thriving lending portfolio is being considered a critical goal for many credit unions.

Now rates are rising, which has yet to cool the housing market, but signs of slowing are showing up. The global supply chain issues have everything from garage doors to computer chips jammed up, affecting everything from C&D loans to mortgages to auto lending. And refis are plummeting, per Freddie Mac.

Attracting Younger Credit Union Members

At present, many members of younger generations are handling their banking and lending business through banks. According to a report from Fiserv, only 9% of millennials claim a credit union as their primary financial institution compared to 74% who are customers of banks. Credit unions will need to work hard to appeal to current and potential younger members, and that will require greater investment in technology and digital services, such as financial wellness tools. Demand for these tools and services are likely to be in more demand than ever in 2022, and that will help credit unions build those lifelong relationships with millennials and Gen Z.

Making More Mortgages

The housing market was wild in 2021 due to the lack of inventory and higher prices. As for 2022, the market still has a way to go before demand balances more appropriately to supply, but a slight increase in newly built homes will help the situation begin to go back to normal. At the same time, second-home mortgages could hold promise for lending portfolios, so take the time to explore the possibility and see if there’s a market for it among your membership.

Coming to a Credit Union Branch Near You

The number of credit union branches have been on the decline since 2008, and during the pandemic, going into a branch was out of the question and online and mobile banking experienced tremendous growth. However, the idea of going to a branch and talking to a live person is not down for the count. People still want to talk to other people, so branches will still have an important role to fill in 2022. Perhaps you may not need as many branches, but it’s still important to keep them open and maintain them.

Yet, even in the branch, members want a high-tech experience. More than three-quarters (79%) of consumers visited a branch in 2021, Wescom Resources Group reported. Welcome them back with open arms and time-saving technology they’ll love that allows your member service reps to provide the attention they deserve – and cross sell opportunities! Learn more about the efficiency and security of Tellergy branch technology.

Extending COVID Relief per NCUA

If your federally insured credit union has been relying on the NCUA’s COVID-19 relief measures, the good news is that the relief measures have been extended and will remain in effect until Dec. 31, 2022. As the president and CEO of CUNA Jim Nussle expressed,

“Thanks to the NCUA board for acting to ensure these relief measures will remain in place through the end of next year, particularly as the pandemic and its effects continue. Extending these modifications continues to allow credit unions the flexibility to continue to meet member needs as they arise.”

Increasing Creditworthiness

Despite the fact that many Americans lost their jobs during the pandemic, delinquencies and credit card balances decreased, giving many people a significant boost to their credit scores. While delinquencies were expected to go back up in 2022, we haven’t really seen that yet. According to TransUnion, despite the end of COVID forbearance and financial support, delinquencies are relatively flat and remain below 2019 levels. there are still plenty of opportunities for credit unions to offer loans to their members with more confidence.

Retaining Credit Union Staff

We’ve all heard a lot about the Great Resignation and how many Americans are thinking about what they want out of life and their jobs, and this is something that credit unions have contended with in 2021 and will continue to do so in 2022. According to Bankrate’s August 2021 Job Seeker Survey, 55% said they are likely to look for a new job in the next 12 months. If credit unions hope to retain their staff, building and maintaining the culture of your institution while also bringing in new innovations and automation to better serve members will play key roles.

A lot is riding on 2022. Credit unions will have to perform a delicate balancing act of maintaining current memberships while finding ways to grow and bring in new members, particularly younger members as the average age of credit union members continues to increase. There’s also the matter of how the various lending markets will change over the course of year as America continues its struggles with the consequences of the COVID-19 pandemic and now the invasion of Ukraine and inflation. 2022 hasn’t been an easy year for credit unions, but this is what we were built for.