Following Rapid Rise in Credit Card Use, More Consumers Now Using Unsecured Personal Loans to Consolidate Debt

New TransUnion study shows that for many, credit card debt relief may only be temporary

A new TransUnion (NYSE: TRU) study, “Debt Consolidation in a Rising Economy,” found that amidst a period of growth in credit card balances and originations, consumers continue to turn to unsecured personal loans as a way to consolidate high interest credit card debt.

The study examined which consumers were turning to unsecured personal loans (UPL) for credit card debt consolidation as opposed to those who used them to refinance existing UPLs, or for other purposes. The study then examined how these groups compared across a number of metrics between April 2021 and September 2022. The metrics included changes in cross wallet credit balances, impacts on credit scores and relative loan performance.

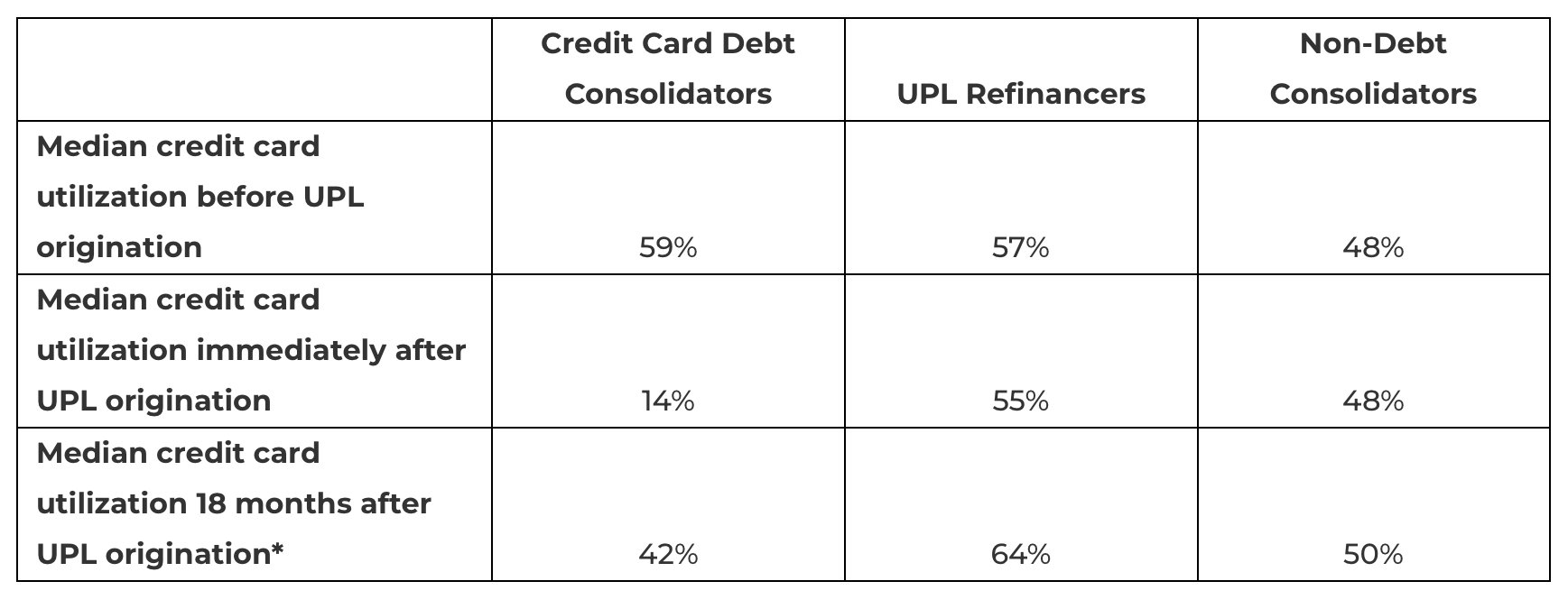

The study found that credit card debt consolidators saw a decrease in their credit card balances of 57%, on average, after consolidating. However, for many credit card debt consolidators, those balances returned close to their previous levels 18 months later. The study also found that the consumers who used unsecured personal loans to consolidate credit card debt were more likely to be in the prime or above risk tiers as opposed to UPL refinancers and non-debt consolidators who were weighted toward below prime.

“As the Fed has raised interest rates in hopes of curbing inflation, many consumers have turned to unsecured personal loans as a way to consolidate their credit card debt to get a lower interest rate,” said Liz Pagel, senior vice president and head of TransUnion’s consumer lending business. “After paying off credit card debt and increasing open to buy on their cards, these consumers not only save on interest over time, but they also see an improvement to their credit scores.”

Credit Card Debt Consolidators Saw Significant Declines in Credit Card Debt Following UPL Origination, But for Many It Did Not Last

Median utilization is calculated over the last 18 months, i.e. April 2021 – Sep 2022

* April 2021 cohort

“Consolidating credit card debt into an unsecured personal loan can be a good option to pay your debt off while freeing up funds in your monthly budget,” said Margaret Poe, head of consumer credit education at TransUnion. “However, it’s important to pair this with changes in spending habits to ensure that the credit card debt doesn’t return.”

In addition to the aforementioned decrease in overall credit card balances, the study found that those consumers who used unsecured personal loans to consolidate their credit card debt saw, on average, an 18-point increase to their credit scores. Prime and above consumers managed to maintain this credit score improvement 18 months later, as opposed to near prime and subprime credit card debt consolidators who saw their scores decline over that period. Across risk tiers, consumers who used loans for consolidation performed better on those loans over time.

These overall credit score changes stood in contrast to UPL refinancers and non-debt consolidators who saw minor declines in their credit scores, which persisted at least 18 months after consolidating regardless of risk tier.

Pagel added, “Lenders would be best served to leverage credit data to identify potential borrowers likely to benefit from debt consolidation or seeking a debt consolidation loan. Additionally, lenders can leverage non-credit-based marketing data to help tailor messaging to identified prospects. When correctly applied, insights from credit and marketing data can lead to better-informed prescreen strategies, as well as stronger approaches to underwriting and marketing messaging that are more apt to resonate.”