North American Migration Map – An infochart by the team at North American Van Lines

Source: North American Moving Services

William Wille, managing editor, The Credit Union Connection

The 2025 National Movers Study is in, and it’s basically saying, ‘Here, hold my beer.’

Americans are on the move, and not in small numbers. And, affordability is driving the U-Haul.

This shift directly impacts credit unions’ membership base, lending portfolio and long-term relevance.

Where Americans Are Moving and What That Means

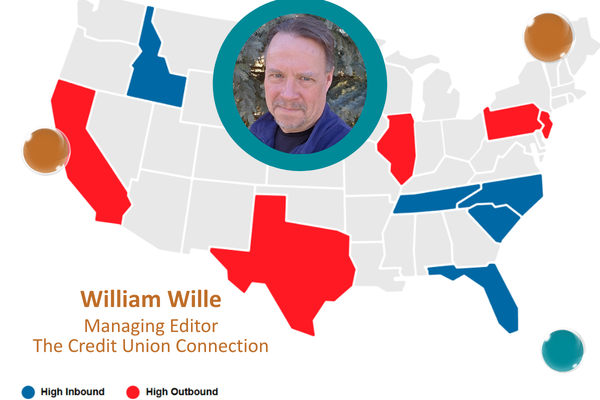

For the second year running, Idaho is the reigning heavyweight champion of inbound moves with South Carolina, North Carolina, Tennessee and Florida following on the victory podium (and have consistently been among the top inbound states since 2020). This inbound migration is driven by a shift toward more affordable, mid-sized markets.

Meanwhile, outbound migration continues to hit historically high-cost states. California takes a top spot for the second year in a row in a contest nobody wants to win. It leads the list of the top five states watching the taillights fade into the distance, followed by New Jersey, Illinois, Pennsylvania and Texas.

Recent data from WalletHub’s 2026 States Where People Spend the Most & Least on Housing Report also confirms that housing costs, mortgage rates and the overall cost of living are forcing the hand of the American consumer.

In states like Hawaii, housing can consume roughly 50% of median income. In California, it’s more than 40%. In New York, renters are shelling out more than 61% of their income on housing. At that point, the math doesn’t work, and relocation is the only solution.

It’s the Great American Shuffle.

The 2024 Election “Exodus”: Loud Talk, Quiet Wallets

After the 2024 elections, the internet was full of people threatening to pack their bags for a state that matched their yard signs. But while people talk about moving for red vs. blue reasons, the actual data say they’re moving for green.

There was no mass political exodus. The uptick in outbound migration has been brewing since 2011.

What’s Actually Driving the Shift

Three forces are converging to reshape where and how people live.

1. Housing Costs Are Breaking the Bank

Compare the math: For example, if a renter from New York or a homeowner from California relocates to Iowa, housing now takes up only 17% of their income. That’s a 33%-44% positive disposable income gap. Financial consumers are relocating across the country to where affordability, space and quality of life are still within reach.

2. The Mortgage Rate Lock-In Effect

Millions of homeowners are still holding onto historically low mortgage rates. That has slowed movement in the short term, but it hasn’t stopped. When life forces a move, those same homeowners are moving to places where their dollars go further, and where homeownership still feels attainable.

3. Affordability Is Redefining Geography

Remote and hybrid work have given people flexibility, but affordability is what’s driving decisions. Cities like Boise, Nashville and Raleigh have become magnets not just because they’re desirable, but because they’re attainable.

What This Means for Your Credit Union

Here’s the uncomfortable question: Are you building your strategy around where your members used to live, or where they’re actually going and who’s coming in? The shift is showing up in five critical areas:

1. Field of Membership

If your charter is tied to a shrinking geographic or employer base, that’s a long-term risk. As members move, your ability to retain and serve them becomes a strategic question rather than an operational one. Are you positioned to grow with your members, or are you confined to where they’ve already left? How is your field of membership changing with the influx of new people from different regional cultures? Can you serve them as is, or do you need to make some changes?

2. Digital Experience

In a migration-driven environment, your digital experience is your retention strategy. When people move from high-density cities to less populated, inbound states, they go from train commuters to two-car households.

And that 44% disposable income gap they just “found” by moving to Iowa? Are you getting your piece of that in deposits and savings?

If your credit union’s digital experience doesn’t make it easy to move that surplus into high-yield savings or doesn’t have a strategy to capture the most common loan product, auto financing, you might not be giving them a sticky reason to remain a member.

3. Branch Strategy

Branches still matter, but context matters more. In high-growth, inbound markets, are you positioned to serve new members effectively? In outbound markets, are you holding onto unnecessary branches? Align your branches with reality.

4. Lending That Reflects Real Life

Housing affordability is the story. Mortgage rates might be easing slightly, but overall affordability remains the major barrier. At the same time, members are navigating relocations, timing gaps between buying and selling and uncertainty around rates. Are your products, such as bridge loans or HELOCs, designed for that reality?

5. Your Value Proposition

A high-income membership is not always a safe membership. The WalletHub data also show that Massachusetts, with the second-highest median household income, ranks third-highest in spending due to energy and mortgage costs. Your most profitable members are often the ones with the most mobility, not just your struggling members. If a member moves 1,000 miles away, why do they stay with you? Out of habit? Out of convenience? Intentionally? If you can’t answer that clearly, they can’t either.

The Path Forward

The map is shifting. Growth markets are changing, and member expectations are evolving. Credit unions that adapt to this reality by aligning their strategies and products while meeting members where they are will grow. Those that stay anchored to legacy assumptions will struggle with the aftermath.