Understanding the challenges younger members face reveals which products are key to serving them

James Chemplavil, Founder/CEO, Salus

The financial health of younger consumers is a difficult thing to nail down. There’s so much information out there, often offered without context. That’s why one of the best ways to assess is to look at a consistent data source and see changes over time. This month, the annual Federal Household Survey results were released, and three key questions highlight things we can’t ignore about younger consumers.

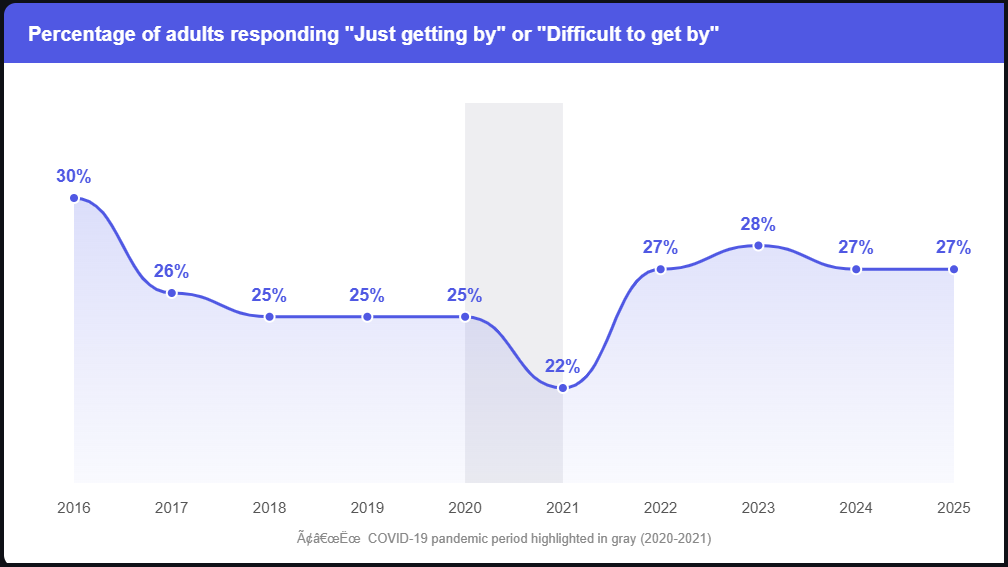

“How well are you managing financially these days?”

Respondents can answer the question in one of four ways: doing comfortably, doing ok, just getting buy, or difficult to get by.

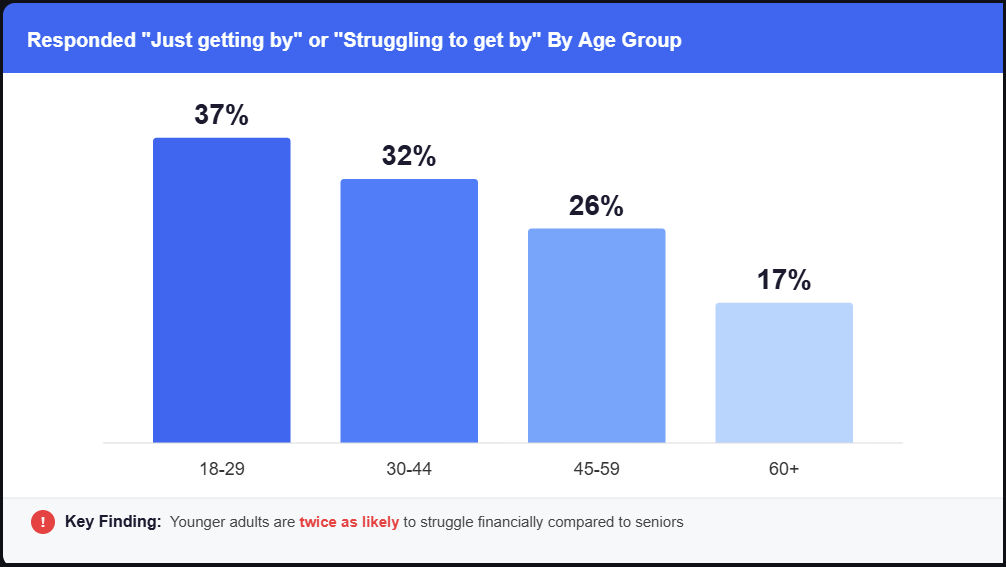

If you look at the headline number, it’s virtually unchanged over the last four years: 27% of people are just getting by or find it difficult to get by. But the responses by generation tell a different story:

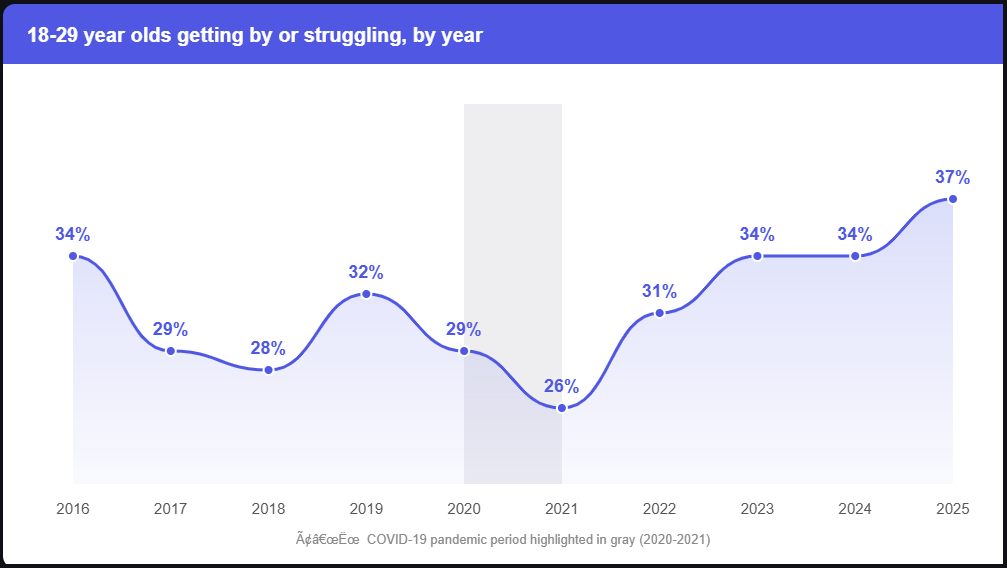

One in three millennials (ages 30-44 here) and Gen Z (ages 18-29) are either just getting by or struggling to get by. In fact, Gen Z responses were twice as high as those from baby boomer (60+) responses. And when you focus just on Gen Z responses:

For Gen Z consumers, things haven’t stayed the same; they’ve been steadily getting worse for the last few years.

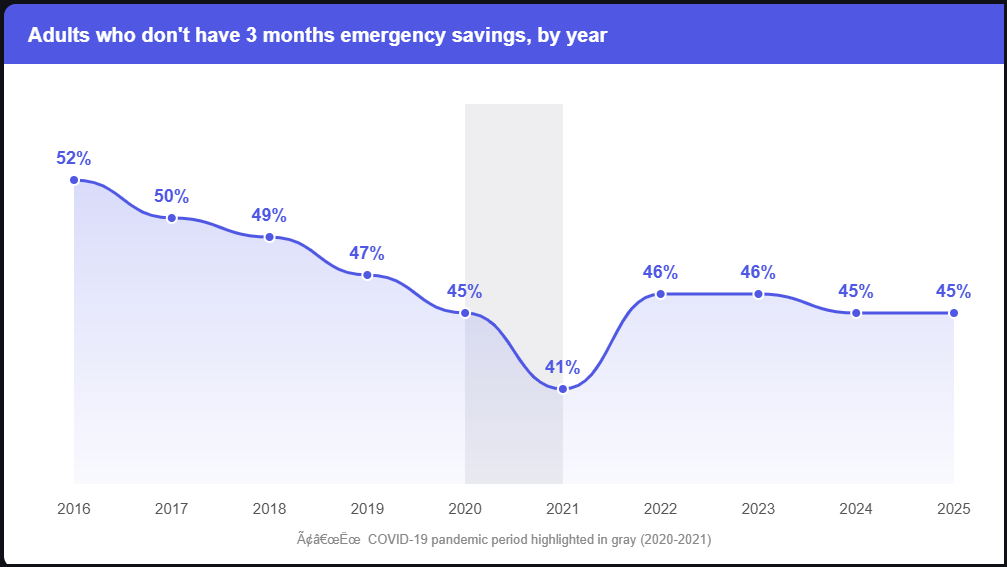

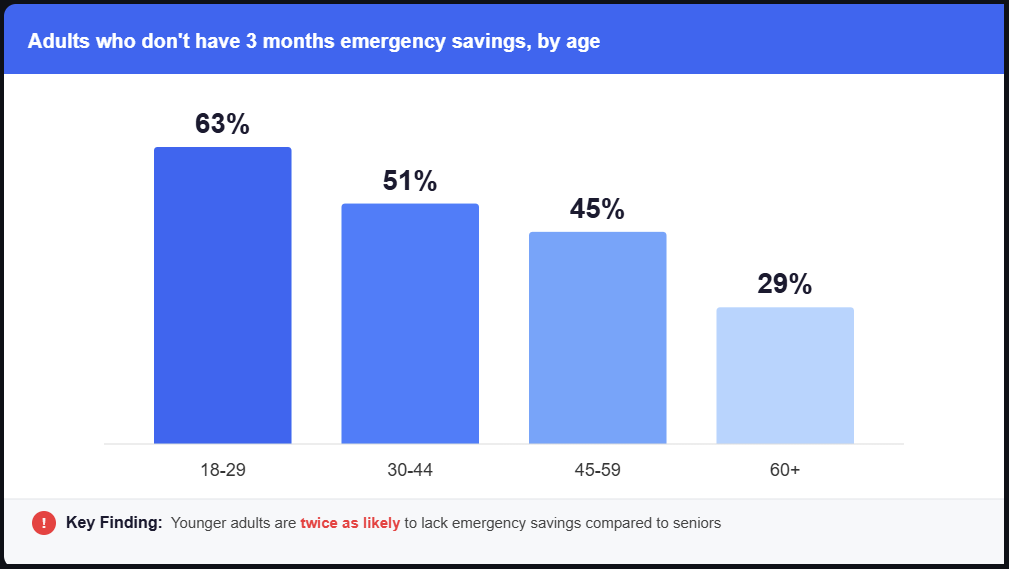

“Have you set aside emergency or rainy day funds?”

For this question, respondents are asked if they have three months of emergency savings set aside.

45% of respondents say they don’t have three months of emergency savings, another number unchanged over the last four years. But the generational responses tell a different story:

Nearly two out of three Gen Z respondents don’t have a three-month emergency savings fund. In fact, the majority of Gen Z and millennial respondents don’t have this emergency savings buffer, while most Gen X and boomer respondents did have savings in place. This means that most younger consumers could be dangerously vulnerable to a financial shock to income or expenses, even one that is short-term in nature.

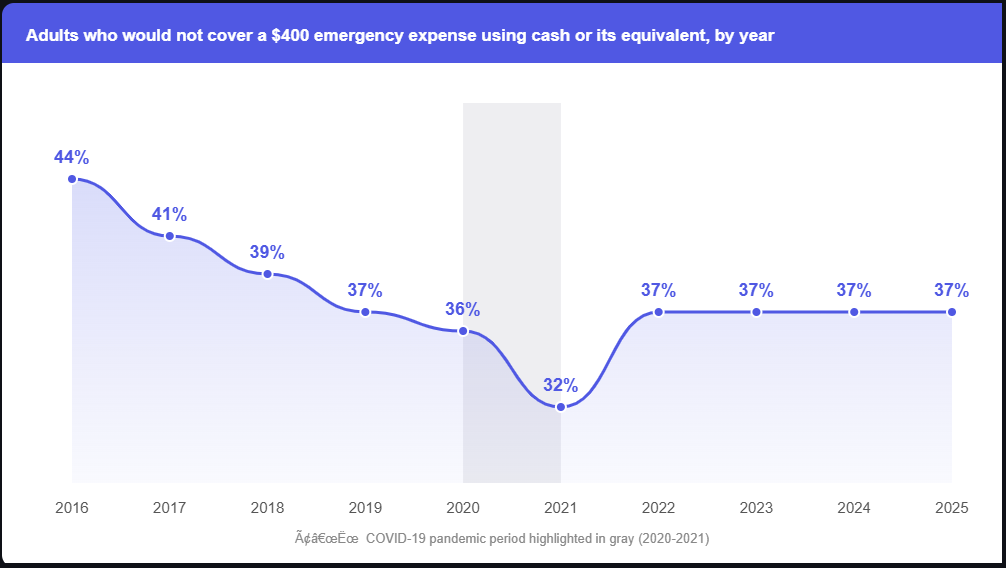

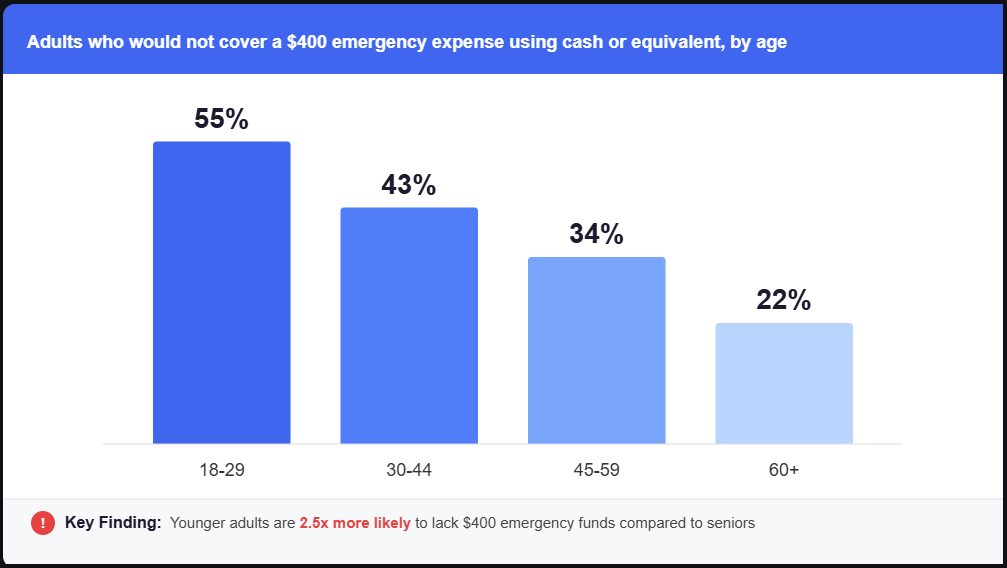

“How would you handle an unexpected $400 expense?”

Perhaps the most popular question from the survey over the years, the overall level of respondents that could not cover an unexpected $400 expense with cash or a cash equivalent has been steady for some time. However, the responses by generation tell a different story:

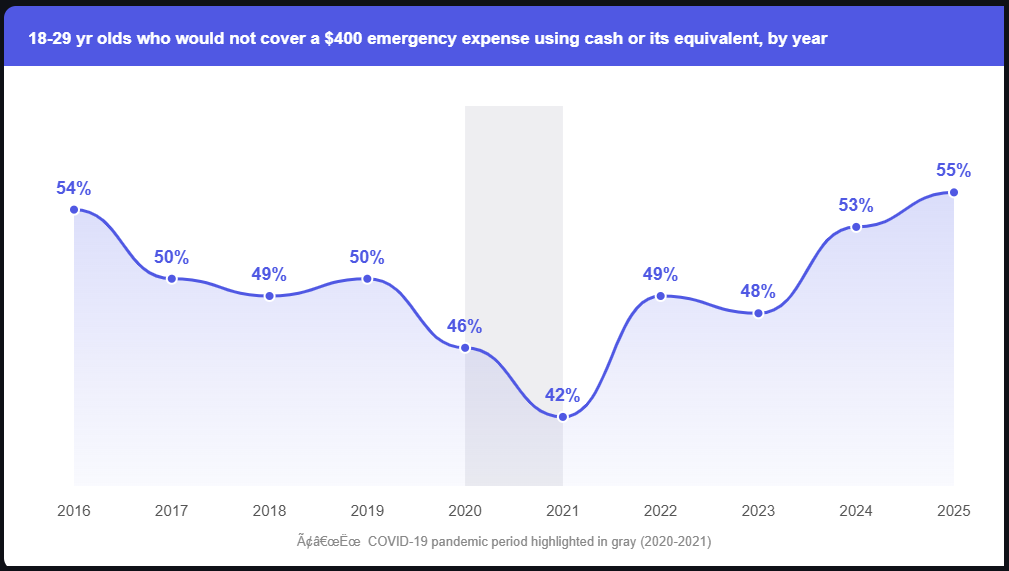

While 78% of older respondents could handle an unexpected $400 expense, most Gen Z respondents felt quite the opposite. 55% of Gen Z would not be able to handle an unexpected $400 expense the same way as their older peers. And this phenomenon is changing quickly:

A few years ago, most Gen Z respondents could handle an unexpected $400 expense. But now, most respondents can’t – and it’s only gotten worse in the most recent data.

What Credit Unions Need To Do

For credit unions that serve (or hope to serve) Gen Z members, they first need to understand how different navigating the world is for younger consumers. They are dealing with day-to-day financial uncertainty that you won’t hear about as often from your members in their 50s, 60s, and beyond. If you want to connect with Gen Z, start by offering products that solve these financial pain points.

Gen Zers and millennials will be valuable members for years to come – so credit unions have a choice: either start connecting with them by offering the products they need or watch them go to the neobanks that will.

Salus can help your credit union turn Gen Z into members for life through products like microloans. Learn more about how we can partner with you.