James Chemplavil, Founder/CEO, Salus

When most people think of alternative finance providers, they likely think about payday loans and other historically predatory lenders. There are other forms of phantom debt today, notably online alternative finance providers. These apps are very popular on app stores, providing advances instead of loans and eschewing the regulations and reporting requirements of the latter. It’s important to know what this could look like for a member.

We analyzed a credit union member’s usage of three alternative finance providers over a six-month period, and here’s what we learned.

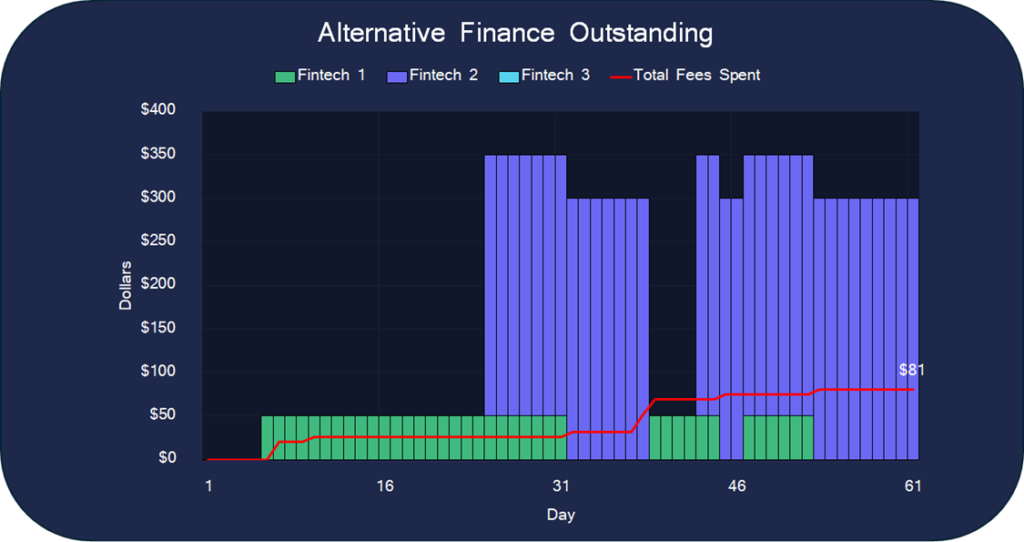

Months 1 and 2

The member starts in the first week by taking $50 from Alt Finance Provider 1. Four days after receiving the advance, $55.89 is repaid to the provider. The member receives another $50 from “Alt Finance Provider 1” the same day they repay the original $50. Much like payday loans, these advances are often rolled into a new one.

By the end of month 1, the member has borrowed the same $50 multiple times, but also starts getting $300 advances from Alt Finance Provider 2. In total, the member uses advances six times in two months, ending the month with $350 outstanding to these providers before fees and expenses.

The member paid $81 in fees and expenses in two months.

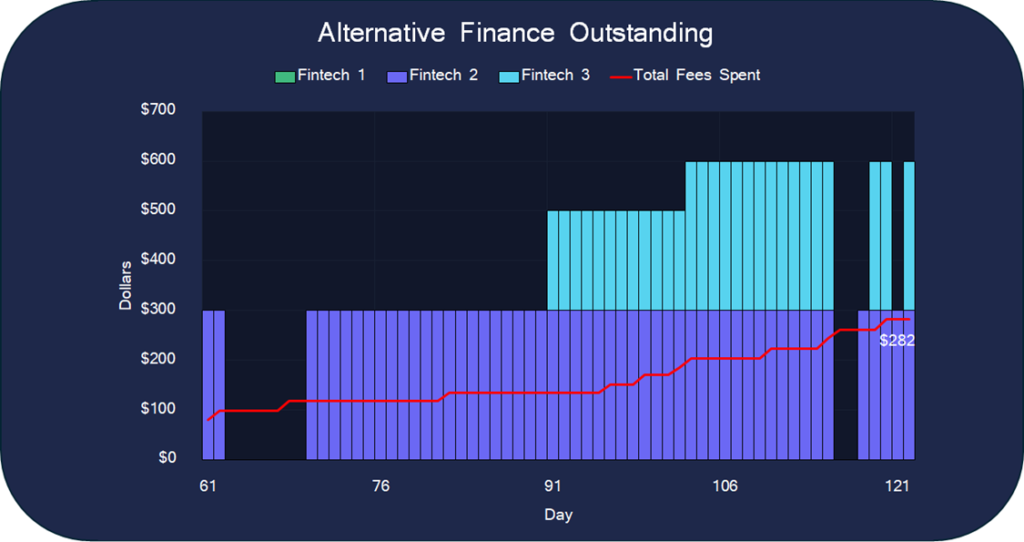

Months 3 and 4

The member uses only Alt Finance Provider 2. The first November transaction is typical: They receive a $300 advance, and 12 days later, the member pays back $316.99 to the provider – and gets another advance days later.

In Month 4, the member starts using Alternative Finance Provider 3 to get a $200 advance. At this point, the member is getting $300 advances from the second provider while still getting $200 advances from the third provider. A few weeks into month 4, the advance amount taken from Alternative Finance Provider 3 increases from $200 to $300.

By the end of month 4, the member has used 10 advances, ending the month with $600 outstanding to these providers before fees and expenses. The member paid $201 in fees and expenses on top of the previous $81.

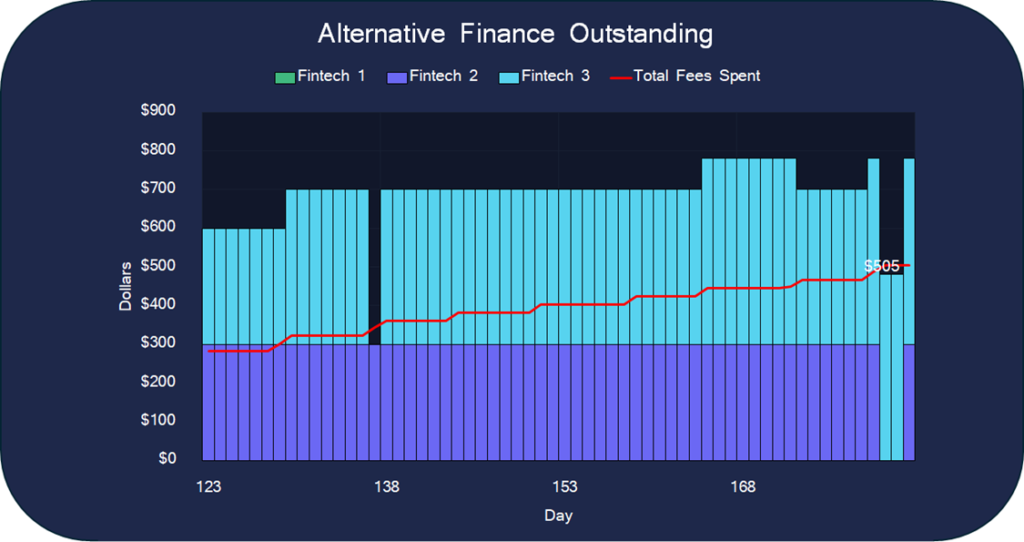

Months 5 and 6

The member is now getting a new advance on the same day they repay an outstanding advance, plus fees and interest. The advances from Alternative Finance Provider 3 have increased from $300 to $400 to $480 by the end of month 6.

In total, the member uses these advances eight times over two months, ending the month with $780 owed to these providers before fees and expenses. The member has paid $223 in fees and expenses in two months.

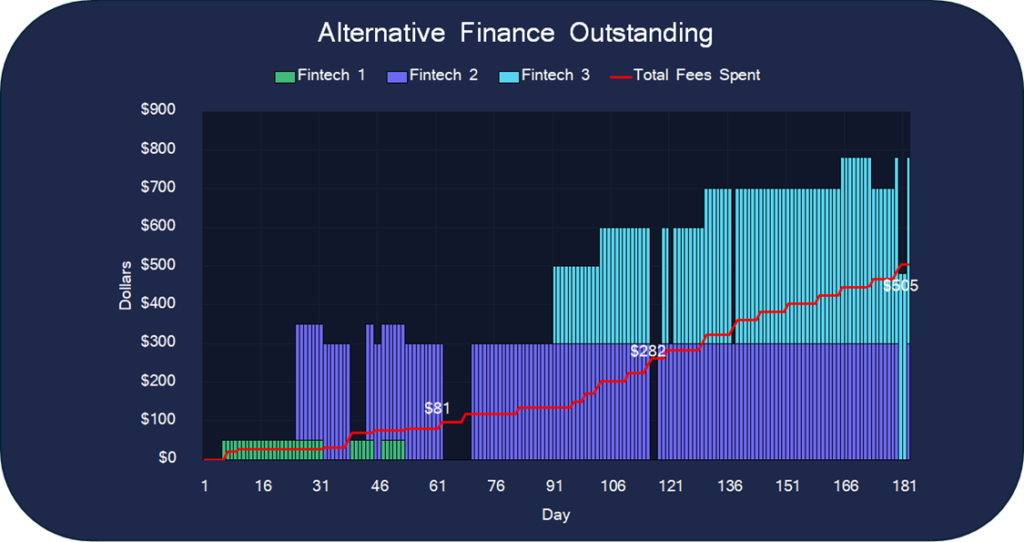

Total Alternative Finance Impact on Member

Over a six-month period, the member received 24 advances totaling $6,780, paying them back plus an additional $505 in fees and expenses. On average, those advances were outstanding for 10.9 days, less than two weeks. Given the short repayment timeframe, what was the average effective annual percentage rate the member paid on those advances?

416% APR

And, at the end of the six months, did these solutions actually solve the member’s problem? They paid a total of $505 in fees and expenses to access these advances, which is 65% of the $780 they still owe. Alternative finance provider fees were a larger part of the member’s ‘debt’ than whatever caused them to borrow six months earlier.

What Can Credit Unions Do?

Credit unions need to be able to answer this member’s call with a better solution. In an alternative world, instead of this member getting into escalating issues with alternative finance providers, they go to their credit union for help.

A 12-month, $800 loan at an 18% interest rate would give the member 12 monthly payments of $73.40 to manage, instead of 24 payments over six months. It would save them $425, or 84% (!) in fees and interest. Credit unions can measure that impact in dollars, but what isn’t measured is how a member’s burden is eased and how that member feels about the credit union helping them in a time of need.

Be Proactive, Not Reactive, And Help Members Thrive

In today’s world, credit union members face two threats from fintechs that provide alternative finance beyond what’s on a credit report. They can use their solution to entice a member to leave the credit union or make a member’s challenging financial situation even worse.

Salus positions your credit union to help members navigate issues like these, with fully automated digital microloans and more that have saved credit union members over $662,000 in fees and interest. Learn more about how we can partner with you.