We asked our highly-targeted audience of LinkedIn followers a question you’ve probably debated at every strategic planning session:

What matters more to members, competitive rates or great member experience?

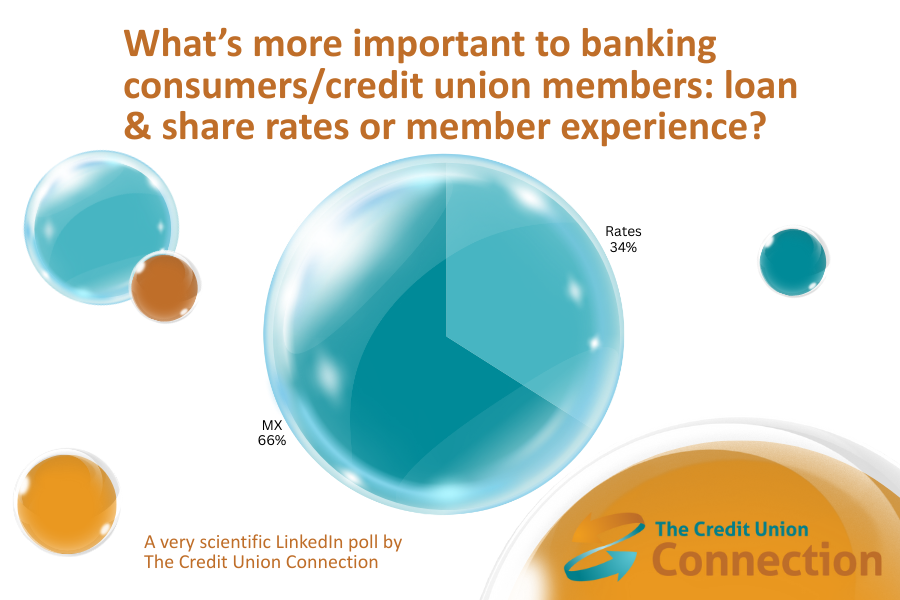

Out of 77 votes on our LinkedIn poll, 66% chose member experience and just 34% said rates were the deciding factor. Fortunately, no one responded, ‘Dunno.’ We did receive two comments:

- There is no “vanilla” CU member.

- D. Both. (which The Credit Union Connection intentionally left out as an option)

Let’s be clear: Rates absolutely matter. And – they’re table stakes.

This poll confirms what you’re probably already seeing in your own data. Rates might attract members, but experience is what keeps them from leaving for the fintech app. The numbers tell the story, as Benjamin Conant below cites Cornerstone Advisors, that more than $2.15 trillion in deposits have migrated from traditional institutions to fintechs. Not because digital banks are crushing everyone on rates, but because they’ve nailed the experience. One-tap payments. Pre-filled applications. Support that doesn’t feel like punishment.

We asked industry experts to break down what this experience-versus-rates reality means for credit unions in 2026. Here’s what they told us.

Preetha Pulusani, CEO of DeepTarget

“While competitive rates are the price of entry, member experience is the true differentiator. In a commoditized market, even a market-leading rate is invisible if it isn’t presented to the right member at the right moment. We have found that when credit unions use data to deliver a hyper-personalized experience- matching specific needs to relevant offers – members prioritize that ease and relevance over rate shopping. A prime example is Georgia United Credit Union, which influenced over $42 million in loan balances not by competing solely on price, but by using AI to ensure the right loan offers found the right members before they looked elsewhere.”

Daniel Ahn, CEO and co-founder of Delfi

“Loan and share rates still matter most because they directly affect members’ financial well-being. Even the best digital experience can’t outweigh the value of affordable credit and competitive returns. But setting these rates responsibly requires strong ALM discipline, ensuring credit unions stay competitive without compromising balance-sheet health.”

Richard Guillot, CEO, BAFS

“While competitive rates and low fees are table stakes to attract members, superior service and high-quality experiences are what drive long-term retention and loyalty. Members expect digital tools that make banking easier, but research shows these tools should enhance, not replace, human service. Credit unions that combine fair pricing with attentive, personalized support are the ones that will truly stand out in today’s market.”

Keith Riddle, general manager, Payfinia

“Credit union members consistently prioritize the member experience over technical metrics like loan and share rates. While competitive pricing remains a foundational expectation for accessing capital and returns, the primary driver of satisfaction and loyalty is the quality of engagement. Members are increasingly demanding seamless, secure, and intuitive digital and in-person interactions that simplify financial management. A truly strong, member-focused experience builds critical trust and fosters deep loyalty, ultimately yielding a far greater and more lasting impact than rates alone.”

Mac Thompson, CEO/founder, White Clay

“While both matter, context is key. For those credit unions focused on indirect lending, where relationships are usually minimal, competitive loan and share rates will often take priority over member experience. However, for members with a full banking relationship, member experience wins. As margins continue to tighten and indirect markets become harder to sustain, many credit unions are leaning into a relationship banking focus, shifting toward deeper member engagement and personalized service. As a recent White Clay survey found, 68% of consumers do not feel truly known by their current primary institution, underscoring both the need and opportunity for stronger member connections. Ultimately, long-term success depends on balancing attractive rates with a member experience that fosters loyalty and trust and shows that they are seen and valued.”

Matt Tomko, CRO, Happy Money

“Both loan and share rates and the member experience are extremely important. While the rates may be what initially attracts the member, retention typically hinges on how well an institution balances the two. A positive member experience – especially seamless digital experiences – has become table stakes for keeping members engaged. The institutions truly standing out are those offering impactful guidance and support for consumers’ biggest financial hurdles. With U.S. households carrying more than $1.23 trillion in high-interest credit card debt, many Americans are actively seeking structured, meaningful alternatives like personal loans to regain confidence and reduce stress. Delivering these solutions with clarity and purpose not only addresses immediate financial strain but also builds trust, which is the foundation of retention. In uncertain times, pairing strong rates with exceptional member experiences drives loyalty, resilience and sustainable growth.”

Denny Howell, COO, Mahalo

“A positive, well-structured member experience is essential when presenting rates and product options. When the experience is confusing, difficult to navigate, or lacking clear guidance, members are far less likely to understand the value behind the rates they’re offered. This can lead to frustration, hesitation, or even complete disengagement. Without an intuitive path that explains what matters and why, members may overlook competitive rates, misunderstand key differences between products, or fail to recognize opportunities that could genuinely improve their financial well-being. A poor experience doesn’t just create inconvenience—it becomes a barrier to comprehension. Members may skip important information, misinterpret product details, or assume everything is complicated even when it isn’t. For neurodiverse members—such as those with ADHD, dyslexia, autism, or processing differences—these barriers can become even more significant. Overly dense text, unclear layouts, or unpredictable flows can make it harder to process information, leading to unnecessary stress and reducing their ability to confidently engage with financial products.”

Eric Gubka, Strategic Partnerships Manager, Member Driven Technologies (MDT)

“While rates will always matter, member experience carries more weight in the long run because it influences every interaction a member has with their credit union. Competitive rates can attract attention, but a seamless, supportive and consistent experience is what builds trust and loyalty, and ultimately keeps members coming back for more in their time of need.

Members want clarity, speed, security and accessibility, and they want to feel understood when they reach out for help. If a credit union delivers that level of experience, they become the primary financial partner amidst a plethora of choices, even in periods when rates fluctuate. Rates may open the door, but experience is what keeps members engaged and committed.”

Alison Heller, Sales Director for Consumer Finance, Equifax

“From my perspective, rates get members in the door, but experience is what keeps them. Most consumers expect competitive pricing, so the difference comes down to how easy it is to apply, how quickly decisions are made and how confident they feel throughout the process. A smooth, transparent experience matters more than a few basis points, especially for younger borrowers who value convenience and clarity.”

Jon Tvrdik, founder & CEO, WaveCX

“From a member’s perspective, rates get attention, but experience earns loyalty. A slightly better rate might attract someone initially, but the experiences that truly matter are the ones that make digital tools intuitive, reduce friction and guide members toward the right decisions. Members want interfaces and tools that anticipate their needs and react in real time while helping them act confidently without extra effort. As more financial products appear across multiple channels, the experiences that turn tools into meaningful solutions will be those that help members make sense of it all through building trust, clarity and convenience in ways rates alone cannot.”

Barry Kirby, co-founder/CRO, Union Credit

“Rates matter, but only after consumers find you. Most never make it that far. Our survey during the government shutdown showed people aren’t avoiding loans; they’re avoiding uncertainty. Only 12% feel very confident about their finances, and they’re not going to dig through websites to compare rates when a clear, convenient offer is already sitting inside an app they trust. That’s where experience wins. It removes steps, answers eligibility questions upfront, and gives members the confidence to act. Without visibility and convenience, even the best rate is invisible. Credit unions that make discovery effortless will earn the right to compete on rates at all.”

Brynn Ammon, president of credit union solutions, Jack Henry

“Loan and share rates have long been a credit union’s bread and butter, but in 2026, member experience is the true differentiator. Competitive rates attract attention – but they rarely sustain loyalty. Today’s consumers expect seamless digital interactions, personalized advice, and proactive support. They want banking that feels intuitive and human, not transactional. Fintechs and big banks are winning because they combine convenience with insight, anticipating needs before they arise. The future belongs to those who seamlessly tie together data-driven personalization, frictionless technology, and empathetic service. Rates may get a member in the door, but experience keeps them and turns them into advocates.”

Edward Vincent, CEO, Lumio Solutions

“While competitive rates are typically seen as table stakes, deep, local relationships differentiate. Equipping front-line colleagues with timely, relevant and actionable intelligence is critical to consistently delivering value during member interactions. This intelligence is predicated on strong data foundations. When information is complete, accurate, and well-organized, credit unions can see member needs more clearly and respond with greater precision. This high-quality interaction builds and reinforces durable loyalty.”

Michelle Bloedorn, CEO, Member Loyalty Group

“When it comes to rates versus experience, the two have become inseparable. Competitive loan and share rates still matter, but they no longer win loyalty on their own. Members increasingly expect experiences that are simple, personalized and responsive, delivered through interactions that anticipate their needs and make them feel understood and supported. Technology plays an integral role, from reducing friction in digital journeys to empowering staff with the insights they need to act quickly and empathetically. Ultimately, members want to feel that their credit union not only offers fair rates, but also genuinely understands and values them. The institutions that succeed will be those that deliver experiences that earn trust, build loyalty and make financial interactions feel human.”

Jennifer Dimenna, VP Product Management, CSI

“Although interest rates are important to consumers when they are buying or improving their home or buying a car, those events are relatively infrequent when compared with the regularity that they access their primary financial institution. When the member experience is easy to navigate, fully functional, accessible from anywhere, and importantly, backed by data, member engagement with the financial institution increases. As credit unions increasingly have the opportunity to leverage AI to anticipate their members’ needs, the member experience will be more personalized, which allows the credit union to transform from a transaction processor to a lifecycle partner. Especially as financial institutions work to attract and retain the younger generations of account holders, personalized, proactive engagement and timely product offers based on member behavior and patterns are key.”

Alisha Stair, Sales Manager for Credit Unions & Banks, PayNearMe

What we’re seeing is that younger members absolutely care about rates, but they vote with their thumbs. If making a loan payment or moving money is harder than sending money to a friend, they’ll gravitate to whoever offers the most effortless, mobile-first experience. A growing share of Gen Z and millennials want to pay loans with stored mobile wallets, receive text reminders with one-tap personalized payment links, and have details pre-filled so they don’t have to remember logins or account numbers. When you meet those expectations, delinquencies fall, support calls drop and loyalty rises.

Competitive rates get members to notice you, but the experience is what turns that pricing into loyalty. Especially for Gen Z and millennials, a slightly better rate still loses if it comes with friction. When credit unions make it easy to pay, communicate clearly and offer flexible paths to stay current, member experience does the work that rates alone can’t. That is a strategy that is much harder for your competitors to undercut.

Benjamin Conant, chief product officer, Alkami

Community banks and credit unions will double down on modernizing account opening to stem deposit outflow to fintechs.

A massive deposit migration is underway. Cornerstone Advisors reports that more than $2.15 trillion in deposits have already left megabanks, regional banks and community institutions for fintechs, and 44% of new checking accounts last year were opened at digital banks and fintech companies.

To compete, every financial institution needs a well-rounded, modern deposit growth strategy.

At its core, that strategy should rest on three pillars: acquiring new deposits, retaining existing deposits, and growing deposits with current account holders. If any one of these pillars is weak, the foundation of the deposit strategy is unstable. Given the massive deposit outflow in the market today, deposit retention and growth among existing account holders are more critical than ever.

In 2026, community banks and credit unions will fight back by delivering frictionless digital account opening experiences, supercharged by technologies like Plaid Layer, that rival the best fintechs, with an enhanced focus on deepening relationships with existing customers and members.

1 thought on “The Verdict Is In: Experience Beats Rates”

Thank you for launching this poll. I found the comments super interesting to read. I look forward to other polls.