James Chemplavil, Founder/CEO, Salus

As credit unions turn the page to 2026, most are looking at strategic planning. It’s a challenging process, trying to distill dozens of opportunities into the ones that will drive the short- and long-term strategic goals.

There’s no shortage of opinions on what solutions are driving member engagement, so how do we tell what’s actually resonating? It turns out, there’s a public source of information sitting right in front of us – app stores.

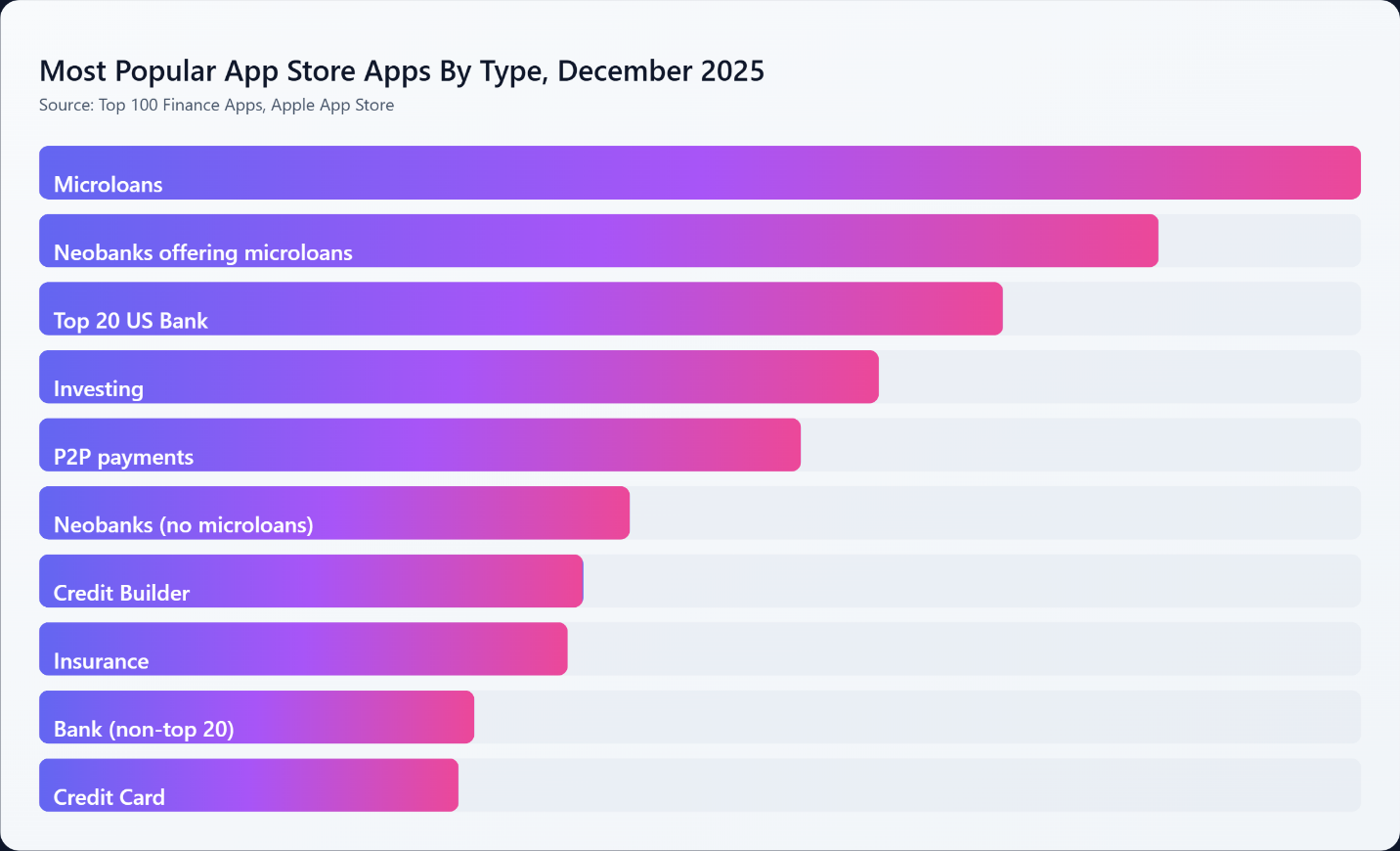

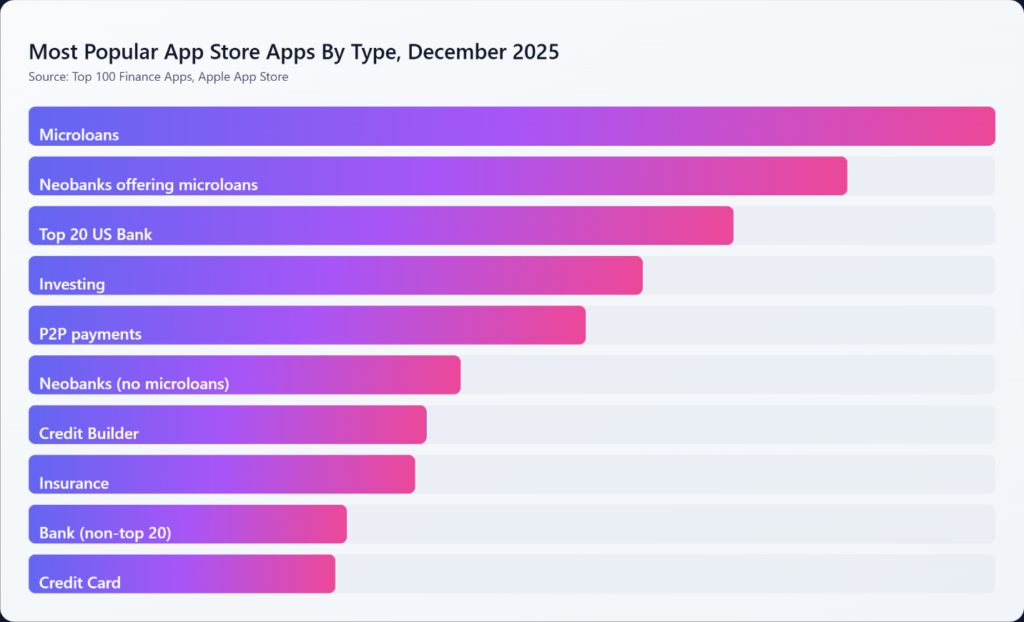

App stores show us what consumers are voting for with downloads and usage. It’s an unbiased look at what resonates with consumers, making it an excellent resource for informing new strategies and initiatives. We looked at the top 100 free finance apps as ranked in the Apple App Store in December 2025. So, what resonated the most with consumers based on their app downloads?

Aside from the types of apps one might expect to see in the top 100 (top 20 US bank apps, credit card apps), there are several types of apps in the top 10 worth digging into.

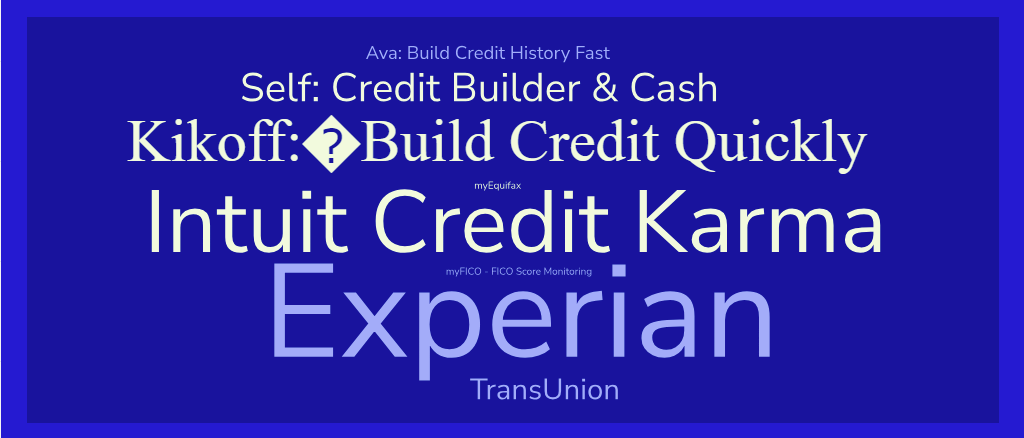

#7: Credit Builder Apps

Eight different credit builder apps appeared in the top 100, with an average ranking of 68. These include the three credit bureaus, FICO and Credit Karma’s apps. But they also include apps by Kikoff, Self and Ava that offer consumers smaller loans, tradelines and other products that help them build credit.

#5: P2P Payments

Eight different P2P payments apps were in the top 100, with an average ranking of 48. The top two were predictably PayPal and Venmo, but several apps are positioned more around global payments, like Remitly, Wise, TapTapSpend, in addition to traditional players like Western Union.

#4: Investing

Eleven different investing apps landed in the top 100, with an average ranking of 61. In this category, newer entrants often outranked traditional service providers. Alinea, a Gen Z-focused investing app founded in 2021, ranked higher than Charles Schwab and Vanguard. Robinhood, which might be considered a mature entrant at this point (founded in 2013), ranked ahead of every investing app except Fidelity. The new entrants were forward-focused on AI-enhanced offerings and access to newer investment assets, such as crypto.

#1: Microloans

19 different microloan apps made it to the top 100, with an average ranking of 62. These apps were primarily focused on providing short-term loans of no more than $600 to consumers. Apps like Tilt (up to $400), Brigit (up to $500), Cleo (up to $250), Klover (up to $400), Grant Cash Advance (up to $300), FloatMe (up to $100) and Possible (up to $500) all offer consumers access to short-term emergency loans.

Turns out, they’re not the only ones. Several of the top apps in different categories are offering the same thing. Self, which has historically branded itself as a credit builder, started offering microloans in 2025. Successful neobanks like Chime, Dave, and Cash App offer members access to microloans in various forms. Why? In their words, to attract and retain Gen Z members.

“We continue to strengthen our short-term liquidity offerings, leveraging our rich data and privileged repayment position as members’ primary account.” – Chime, 3rd quarter earnings call

Takeaways

Based on the apps being downloaded and used last month, consumers were looking for specific solutions to solve their problems. In the data, four types stood out: credit building, peer-to-peer payments, investing and short-term microloans. Consumers solved their need in one of two ways: They either went with a standalone app that solved their problem, or they chose a financial services app that included their solution. Neobanks that offered microloans were twice as popular as those that did not.

Two critical pieces of information surface from the data. First, members have problems they need to solve and are actively seeking solutions. Second, and more importantly, the institutions that can provide that solution can attract and retain those members far more easily. That’s the strategic imperative for credit unions in 2026. Meet members where they are by offering them a solution they need today, so you can help them grow into the products and services that credit unions have excelled at for decades.

Salus can help your credit union turn Gen Z into members for life through products like microloans. If you’re ready, learn more about how we can partner with you.